Key takeaways

• Retail loss prevention is now an engineering problem, not a guard-and-mirror problem. US shrink hit $112.1B in FY2022 (1.6% of sales) in the last full NRF survey before the federation retired it in 2024. The recoverable slice sits in software.

• Self-checkout is the hole in the bucket. One 2023 study measured SCO shrink at about 3.5% of sales versus 0.21% at staffed lanes — roughly 16× worse per dollar. Five AI use cases cover most of what you can win back.

• The 2026 build is a six-layer edge stack. Cameras, an edge AI box, detection models (YOLO26 plus a tracker), POS event correlation, an operator triage queue, and POS integration. Edge-first, because streaming every camera to the cloud breaks the unit economics fast.

• Privacy is an architecture decision, not a disclaimer. Illinois BIPA still carries $1,000–$5,000 statutory damages, though a 2024 amendment caps accrual at one violation per person. Design for behaviour, not identity, and most of the exposure disappears.

• Custom beats turnkey once you pass roughly 25 stores. Per-lane vendor subscriptions from Everseen, Sensormatic or Trigo are quick to start and expensive to scale. A first store typically pays back in 4–9 months either way.

What is retail loss prevention?

Retail loss prevention is the set of people, process and technology a retailer uses to stop preventable loss of inventory and cash — theft, fraud and error — before it eats margin. The umbrella term for that loss is shrink (or shrinkage): the gap between the inventory a store’s books say it has and the inventory actually on the shelf. Historically loss prevention meant guards, mirrors, electronic article surveillance (EAS) tags and a security-camera wall nobody watched. In 2026 the centre of gravity has moved to software that watches the cameras for you and cross-checks them against the point-of-sale.

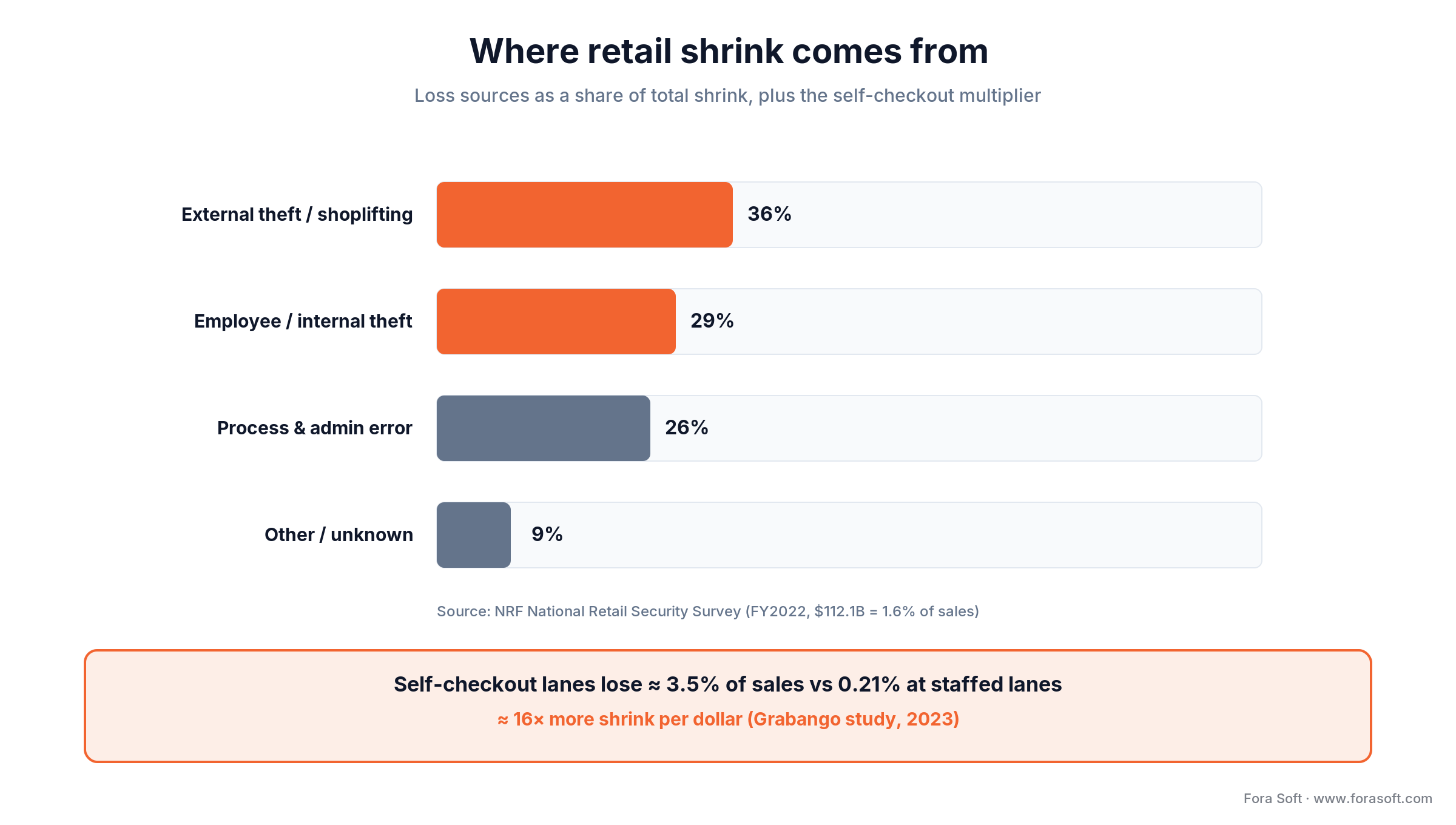

Shrink splits into four buckets, and the split matters because each bucket needs a different tool. External theft (shoplifting and organized retail crime) is the largest. Internal or employee theft is second. Process and administrative error (miscounts, pricing mistakes, receiving errors) is a bigger share than most operators expect. A small remainder is unknown. A serious loss-prevention programme addresses all four, and this playbook shows how AI-driven video and POS analytics attack each one.

We wrote this for the people who have to make the call: loss-prevention directors, security-tech VPs and operators running 15 to 500 stores who are deciding whether to buy a vendor subscription, build a custom system, or run a hybrid. It is a builder’s guide, not a tips listicle. Every number carries a year and a source, and where the honest answer is “it depends,” we say what it depends on.

Why Fora Soft wrote this playbook

Fora Soft has built video and computer-vision software since 2005 — 250+ projects across 21 years, with a team of about 50 engineers who specialise in real-time video, streaming and AI on video. Our surveillance credentials are not theoretical. We engineer custom computer-vision surveillance systems, and our work on VALT — a video-recording and management platform used by 770+ organizations and more than 50,000 active users — taught us what production video at scale actually demands: fleet management, storage economics, retention policy and audit trails that hold up in an investigation.

Retail loss prevention is that same stack pointed at a store: cameras, edge inference, object detection and tracking, and event correlation, wrapped in a privacy posture that survives a lawyer’s review. It is the kind of system our AI integration practice ships. The hard parts are not the models. They’re the POS integration, the false-positive curve, and the operator experience that decides whether store staff trust the alerts or mute them. That’s the ground this guide covers.

The patterns below also reflect the public record: the NRF security research, the Everseen, Sensormatic and Trigo vendor materials, the Hailo and NVIDIA Jetson technical briefs, and the Illinois BIPA case law that reshaped retail-AI architecture between 2023 and 2026. Where our engineering view differs from the marketing consensus, we flag it and say why.

Sizing an AI loss-prevention build?

Send your store count, camera fleet and six months of shrink data. We’ll come back with a use-case map and a per-store ROI estimate. Free 30-minute scoping call.

The 2026 shrink numbers behind the budget

Shrink reached $112.1B in fiscal 2022, or 1.6% of sales, up from 1.4% the year before. That figure comes from the NRF National Retail Security Survey, which the federation then discontinued in 2024 over methodology concerns. So $112.1B is the last full industry shrink number on the record, and anyone quoting a bigger, newer, precise dollar total is guessing. What NRF still publishes is the Impact of Retail Theft & Violence report, and its 2025 edition is where the current signal lives.

That 2025 report found shoplifting incidents up 18% in 2024 versus 2023, and threats or violence during theft events up 17%. Organized retail crime has gone transnational: 67% of surveyed retailers reported an ORC group from outside the country involved in thefts against them, and ORC crews have branched into phone scams, e-commerce fraud and cargo theft. The survey covered 70 companies representing 168 brands and $1.3 trillion in sales, so it speaks for a real quarter of the industry.

Figure 1. Where shrink comes from, and why self-checkout is the outlier worth engineering against.

Walmart, Target and Kroger have run AI loss prevention for years. The 2026 adoption wave is mid-market: the 30-to-200-store regional chains that cannot staff a loss-prevention team the size of a national retailer’s, but now face the same organized crews. For them the maths finally works, because edge hardware got cheap and the alternative (more shrink, more staff) got expensive.

Seven retail loss prevention strategies that work

Before the architecture, the strategy. A good loss-prevention programme layers cheap deterrents under expensive analytics, so you are not paying for computer vision to solve a problem a $4 lock solves. Here is the stack we recommend, from foundation to frontier.

1. Deterrence and store design. Sightlines, lighting, product placement, locked cases for high-theft SKUs, and EAS gates at the door. Old-school, still the cheapest dollar-per-loss-prevented you will spend.

2. POS exception reporting. Mine the transaction log for refund fraud, voids, no-sales and manual price overrides. This needs no cameras and often finds the first real money.

3. Self-checkout monitoring. Camera vision per lane, matched to the scan feed, catching the ghost-scan and the produce-code swap. The highest-yield AI use case in grocery.

4. Behavioural video analytics. Detect concealment, loitering at high-value aisles and coordinated group movement — without storing anyone’s face.

5. Receiving and back-of-house controls. Cameras and document cross-checks at the dock, where a single missed pallet is four figures of shrink.

6. ORC intelligence sharing. Feed confirmed cases into industry networks so a crew hitting five of your stores gets caught as one pattern, not five isolated reports.

7. Staff training and incentives. The camera surfaces the event; a trained attendant decides. Tooling without an operator process is shelfware, and we’ve watched it happen.

Five AI use cases that drive most of the value

Strategies 3 through 5 above are where computer vision earns its keep. Broken out, they become five AI use cases that cover roughly 80% of the recoverable shrink in grocery, c-store, mass merchant and pharmacy. Each has its own camera-and-model footprint, its own ROI shape, and its own privacy posture. Build the programme around use cases, not around the cameras you happen to own.

Use case 1 — Self-checkout sweet-hearting

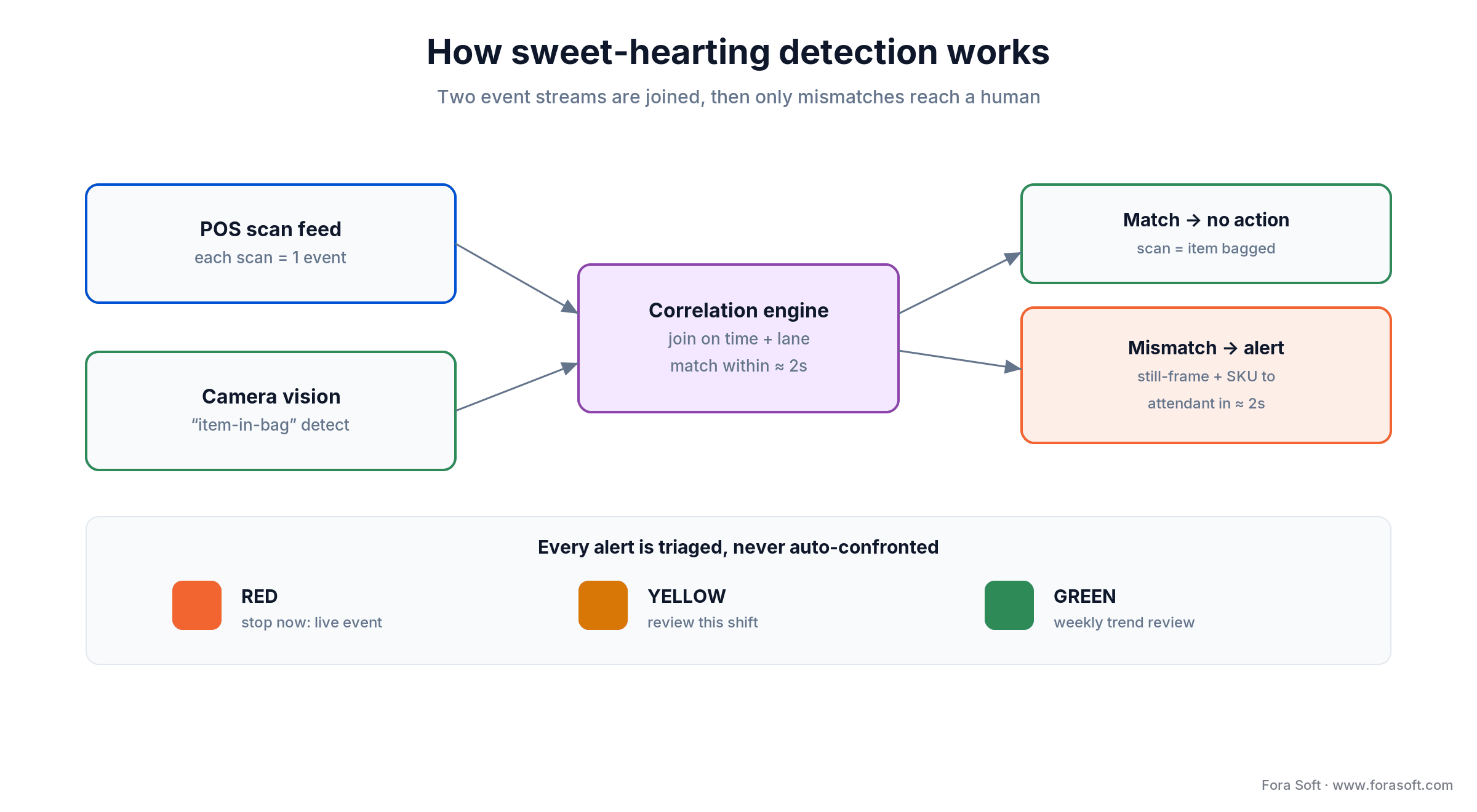

Sweet-hearting is the catch-all for self-checkout fraud: the “ghost scan” where a shopper passes an item over the scanner without registering it, the “banana trick” where an expensive item is weighed or typed in as a cheap one, the low-PLU produce swap, and simply bagging without scanning. Most stores treat honest mistakes and deliberate theft together, because the operational response is the same: surface it to an attendant, let a human decide.

Why it matters so much: one 2023 Grabango study put self-checkout shrink near 3.5% of sales against 0.21% at staffed lanes — about 16× more loss per dollar — with 6.7% of SCO transactions showing at least some partial shrink versus 0.32% at cashiers. The architecture is an overhead camera per lane plus event correlation with the POS scan feed: every scan should match an “item went into the bag” detection, and every mismatch pages the attendant within about two seconds, with a still frame and the SKU.

Figure 2. Two event streams join on time and lane; only the mismatches reach a human.

Reach for SCO sweet-hearting detection when: self-checkout is more than 25% of trips, SCO-lane shrink runs above 1.5% of throughput, or attendants can no longer eyeball every flag. This is usually the first use case to ship because the ROI is the clearest.

Use case 2 — Exit theft

Exit theft is the broader bucket: a shopper walks out with items in a cart or on their person that were never paid for. Detection runs as a camera pipeline at the door, comparing what is leaving against the receipts closed at the registers in the previous window. The false-positive cost here is brutal, because confronting a paying customer is a brand and legal disaster. So the 2026 model never confronts anyone through automation. It surfaces the event to a loss-prevention officer with full video context, and the human makes the call.

Honest-mistake handling is baked in. The shopper who forgot a coupon, who put a bottle in their bag meaning to pay, who got distracted by a kid — the system flags it, the officer investigates without accusation, and the operations team tunes the threshold over weeks. Get this wrong and you train staff to ignore the tool. Get it right and exit theft becomes a quiet, steady recovery.

Use case 3 — Receiving and back-of-house

Receiving errors and back-of-house loss are the process-and-admin slice of shrink, and they are quietly large. The patterns: pallet miscounts, vendor short-shipments, diversions during unloading, and outright theft off the loading dock. Detection pairs overhead and side cameras at the dock with the receiving-document flow (direct-store-delivery or warehouse-managed) for a cross-check between what the paperwork says arrived and what the camera saw come off the truck.

This use case earns its place for two reasons. The per-event impact is high, since a single missed pallet is four figures of shrink. And it has the lightest privacy footprint of the five, because the surface is operational: you are watching goods and documents, not shoppers’ faces. For chains nervous about the legal side, receiving is often the safest place to prove the technology.

Use case 4 — Employee misconduct

Employee theft is the second-largest shrink contributor and the most operationally sensitive one. The patterns are refund fraud (a refund with no return), discount abuse, void and no-sale exploits, manual-PLU entry of expensive items as cheap ones, and straight cash-drawer theft. Most of it lives in the POS log before it ever touches a camera, which is why exception reporting is the entry point.

Detection runs at the register and back-office camera level, paired with POS-event analysis where refunds, voids and manual discounts get flagged for video review. The sensitivity here is extreme: wrongly accusing a long-tenured cashier is an HR catastrophe and, in some states, a lawsuit. So build the system to surface patterns over time — repeated anomalies at one register, statistical outliers across a shift — rather than firing a per-event alert at a manager. The output is an investigation lead, never a verdict.

Reach for pattern-based employee monitoring when: POS analytics alone confirm refund or void abuse, shrink concentrates at specific registers, and HR or employee-relations leadership has signed off on the process in advance. Never deploy this one quietly.

Use case 5 — Organized retail crime

Organized retail crime is the high-loss tail. Crews target high-value, easy-to-fence SKUs (laundry detergent, baby formula, OTC medicine, electronics, designer apparel) and move them through online marketplaces. Per the NRF 2025 report, 67% of retailers saw a transnational ORC group in their thefts over the past year, and the crews have diversified into e-commerce fraud and cargo theft alongside the shelf.

Store-level detection looks for ORC-pattern behaviour: fast concealment in target aisles, multi-person coordination, repeat visits across stores, and vehicle patterns in the lot. The real payoff comes from sharing confirmed cases — with proper consent and contracts — into industry networks and law-enforcement channels, so a crew working a region surfaces as one linked pattern instead of a dozen unconnected incidents. This is where behavioural detection and cross-store data beat any single-camera product.

Reference architecture — the six-layer stack

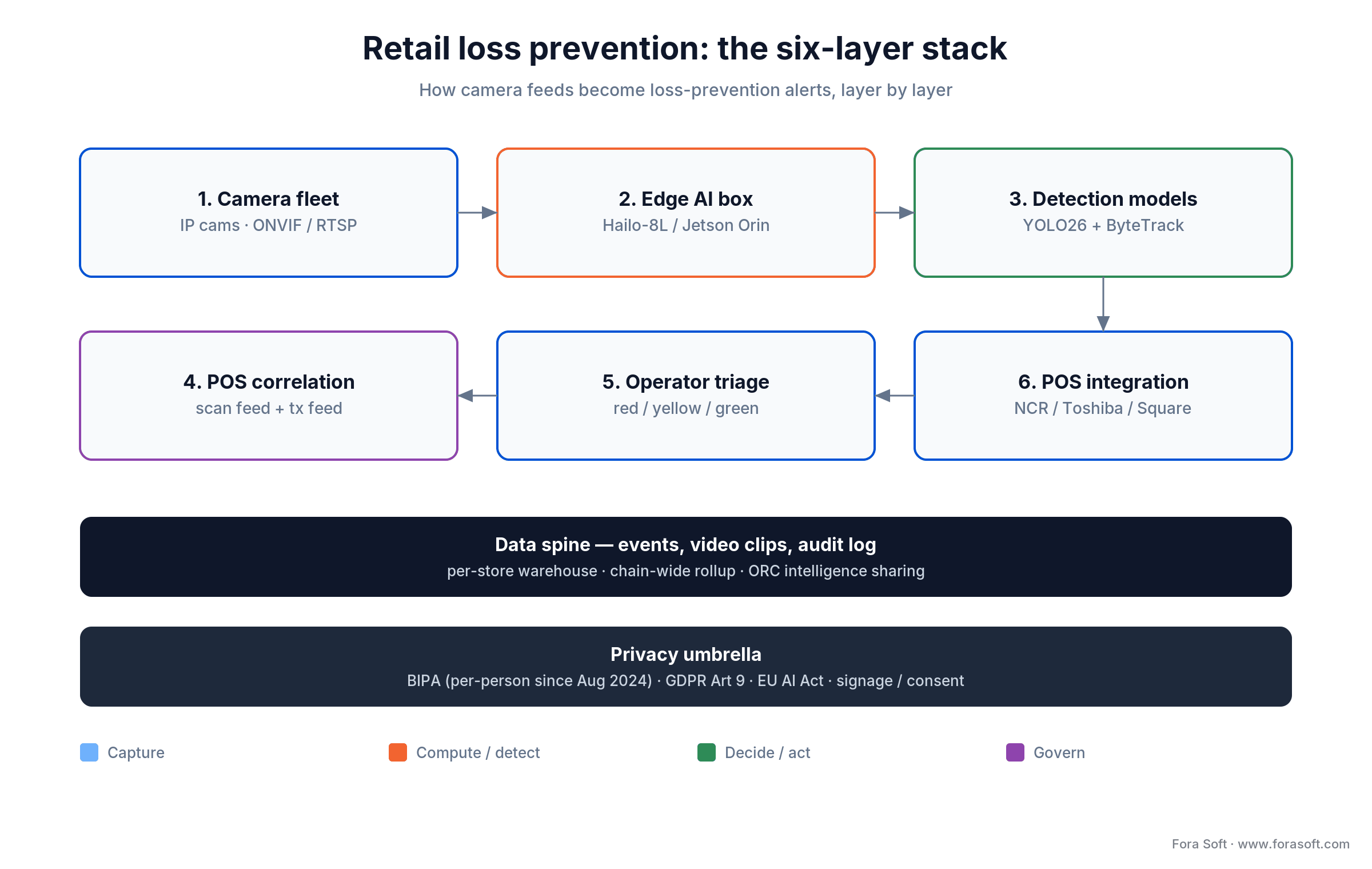

Across the surveillance and computer-vision systems we’ve shipped, a retail loss-prevention build collapses to six layers. The shape holds whether you are working with an existing IP-camera fleet and a legacy NVR or installing a fresh edge stack from scratch. The point of naming the layers is that each one is a separate decision with its own cost, risk and vendor options — and the expensive mistakes come from treating the whole thing as one black box.

Figure 3. The six layers, the shared data spine underneath, and the privacy layer that wraps all of it.

Layer 1 is the camera fleet, usually reused via ONVIF or RTSP rather than ripped out. Most chains already run Axis, Hanwha, Bosch or Avigilon cameras; new installs are limited to overhead-per-lane and dock views where coverage is missing. Spec 5MP-plus sensors with wide dynamic range for the ugly lighting a retail floor throws at you. Bandwidth is the trap: H.265 from a dozen cameras to one edge box is fine, H.264 from two dozen starts to choke. Our guide to modern VMS architecture covers the video-management surface this layer plugs into.

The edge AI layer — Hailo vs Jetson

Cloud inference per camera breaks above about four cameras: you pay tens of dollars per camera per month in compute that an edge box swallows for a one-time cost amortised over years. So layer 2 is an on-prem AI box, and the 2026 choice is mostly Hailo versus NVIDIA Jetson. The Hailo-8 delivers up to 26 TOPS at around 2.5W typical, and the Hailo-8L up to 13 TOPS for lighter loads. NVIDIA’s Jetson Orin Nano now reaches up to 67 TOPS in Super Mode (JetPack 6.2, late 2024), and the Orin NX up to 157 TOPS, at 10–40W.

The trade is power and framework breadth against raw throughput. Jetson gives you the widest model support and the most headroom; Hailo gives you cooler, cheaper, lower-power boxes that are perfect when the model set is locked and the back room runs hot. A typical per-store spec is one Orin NX or a couple of Hailo-8L boxes for 12–20 cameras, in a fanless industrial enclosure, on a dual VLAN (cameras plus management), with a UPS for the power cuts every retail back room eventually sees. Build a remote-management plane over something like WireGuard so you can patch the fleet without a truck roll.

Reach for Hailo over Jetson when: the back-room thermal budget is tight, the model set is fixed to a handful of detectors, and you want the lowest per-store hardware cost. Reach for Jetson when you expect to add models, run heavier trackers, or want CUDA tooling.

Detection models and POS correlation

Layer 3 is the models. The 2026 baseline is a YOLO-class object detector plus a tracker. YOLO26, which Ultralytics shipped in January 2026, is the current state of the art: an NMS-free, edge-first design with up to 43% faster CPU inference than YOLO11, which matters when you are running on a 13-TOPS edge chip. YOLO11 (September 2024) is still a proven, widely deployed fallback. Pair either with a tracker like ByteTrack or BoT-SORT to follow individuals through the store at 10+ fps and catch concealment. RT-DETR is the transformer alternative when you need it. A COCO-pretrained model out of the box is not enough; you fine-tune on retail footage — cart contents, shelf SKUs, scan-versus-no-scan motion, cashier hand poses. Budget 30–60 hours of labelled in-store video per detector class, with 5–15% held out for evaluation. Our earlier work on anomaly detection in surveillance feeds the unsupervised side of this, and our primer on AI for video engineering covers the fundamentals of running models on video.

Layer 4 turns vision into value: event correlation with the POS. Every scan, void, refund and manual PLU on the register becomes an event; every “item in bag,” “item left cart” and “person at exit” detection on the camera becomes another. The correlation engine joins them on time and lane and produces a tiered alert. The pattern is a per-store streaming pipeline (Kafka or Redpanda for events, a stream processor or a lean per-store service for the join) plus a rules layer that encodes “match within two seconds” or “more than three mismatches in thirty minutes.” The POS feed is the hard integration; the vision side is the easy one.

Operator triage — the human layer

Layer 5 is the triage queue, and it decides whether store staff love the system or mute it. Three tiers work in practice. Red is immediate: a live sweet-hearting event an attendant can still stop. Yellow is review-this-shift: a refund anomaly a manager checks by lunch. Green is trend: the loss-prevention team’s weekly look at which registers and stores are drifting. Route by severity, not volume, or you bury the one alert that mattered.

Ship every alert with a 6–10-second clip, the POS context, a suggested action, and a one-click “true / false / inconclusive” button that retrains the ranking. That feedback loop is what drives the false-positive rate down over months; without it the system rots and trust with it. This is the layer teams underinvest in most, and it is the one that determines adoption. Layer 6, POS integration, is covered in its own decision below because it drives the timeline more than the AI does.

Privacy and the law — BIPA and the EU AI Act

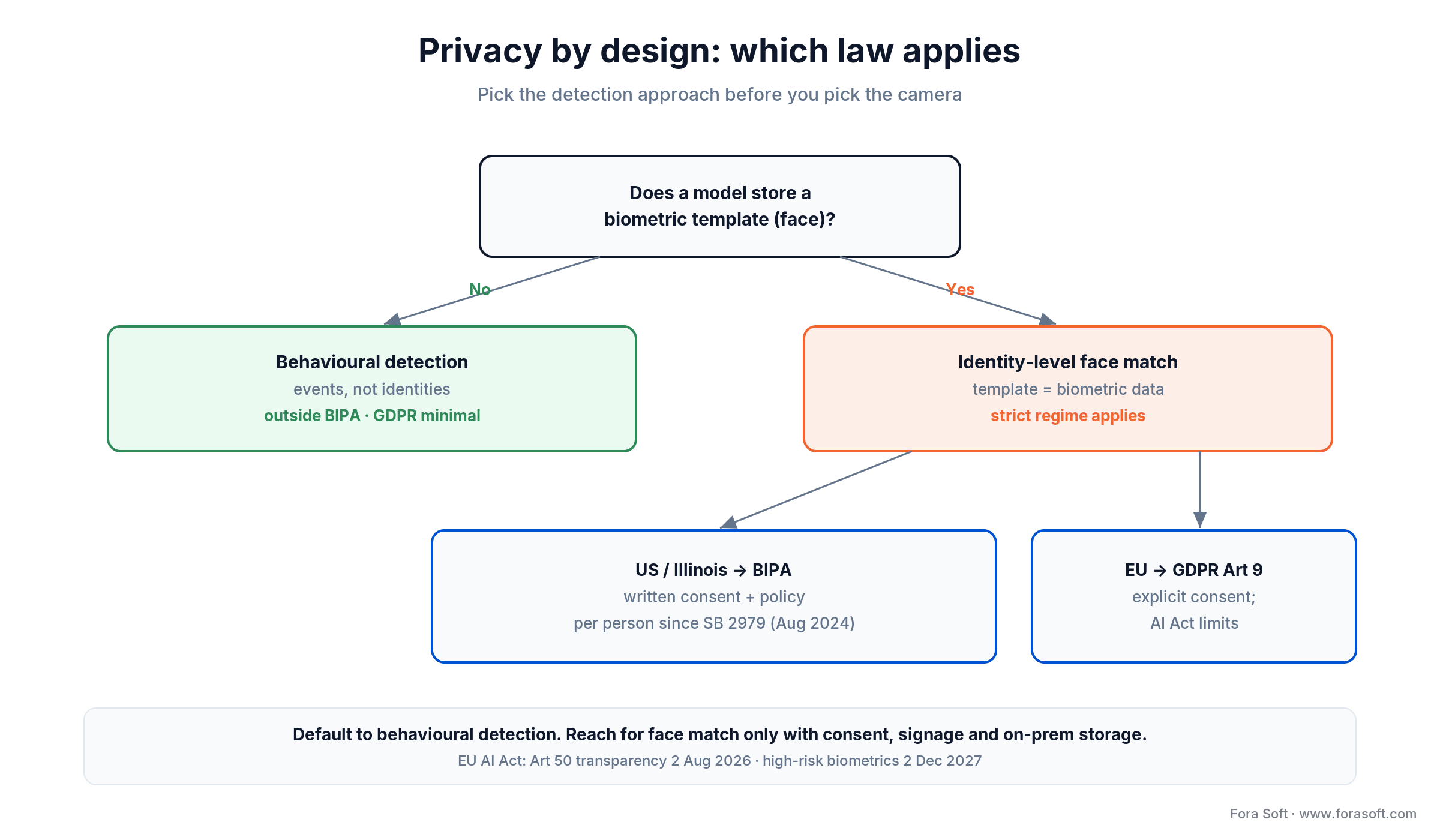

Privacy is the axis that decides whether your programme survives two years, and the single best architectural move is to detect events, not people. In the US, the Illinois Biometric Information Privacy Act (BIPA) sets statutory damages of $1,000 for negligent and $5,000 for reckless or intentional violations. For years the scary part was accrual: after Cothron v. White Castle (2023), each scan counted as a separate violation, and White Castle faced an estimated $17B. Illinois then amended BIPA in August 2024 (SB 2979): a violation now accrues once per person for the same collection method, and electronic signatures count as written consent. That cuts exposure by orders of magnitude — but the consent and policy duties still bind, and Texas, Washington and others have their own biometric statutes.

The clean answer is behavioural detection: loitering, rapid concealment, coordinated movement. It stores no biometric template, so it sits outside BIPA and keeps GDPR light. Where you genuinely need face-based identification — recognising a repeat ORC offender, say — put it behind explicit signage, a written retention-and-deletion policy, template hashing, and on-prem storage only.

Figure 4. One question — does a model store a biometric template? — sets your entire compliance path.

In the EU the map is different. The EU AI Act prohibitions in force since 2 February 2025 ban real-time remote biometric identification in public spaces for law enforcement (with narrow carve-outs) and outright ban biometric categorisation that infers sensitive traits — the latter does hit retail analytics. A retailer’s own face-recognition-for-security use is governed mostly by GDPR Article 9, which treats biometric data used to identify someone as special-category and demands explicit consent or another tight legal basis. The Act’s transparency duties apply from 2 August 2026 and its high-risk rules, including biometrics, from 2 December 2027. Translation: in Europe, behavioural-only is not just safer, it is close to mandatory for retail.

Worried the privacy posture will bite you later?

We design behavioural-first detection that stays clear of BIPA and GDPR traps. Bring your jurisdictions; we’ll map the compliant architecture with you.

Loss prevention software and vendors compared

The retail loss prevention software market splits into turnkey vendors and custom builds. On the vendor side, Everseen has the deepest self-checkout sweet-hearting library and the strongest Tier-1 grocer references. Sensormatic (Johnson Controls) bundles EAS hardware with its Sensormatic IQ analytics. NCR Voyix ships Halo alongside its self-checkout estate. Veesion focuses on gesture and concealment detection. And the space keeps moving: Trigo launched a computer-vision loss-prevention product in June 2025 that matches items picked up against items scanned, and GK Software acquired the CV startup Nomitri in January 2025 to strengthen self-checkout fraud detection.

Here is the honest trade-off, with where each option wins and where it breaks.

| Option | Best for | Where it wins | Where it breaks |

|---|---|---|---|

| Everseen | Tier-1 grocery SCO | Deep sweet-hearting model library, proven at scale | Per-lane subscription, black-box thresholds |

| Sensormatic IQ | EAS-first apparel & mass | Hardware + analytics in one dashboard | Heaviest to customise per chain |

| NCR Voyix Halo | Existing NCR estates | Native POS integration, fast start | Locks you to the NCR stack |

| Veesion / Trigo | Concealment & SCO match | Focused, modern CV, quick pilots | Narrow scope, still per-lane pricing |

| Custom build | 25–200-store chains | Owns thresholds, data and privacy posture; scales without per-lane fees | Up-front engineering; needs an integrator |

Reach for a turnkey vendor when: you run under ~15 stores, want a single self-checkout module live in weeks, and are happy to accept the vendor’s thresholds. Reach for custom when the per-lane fee starts crowding out the savings.

Cost model — per-store economics

Here is the per-store cost shape for a custom edge build that reuses the existing camera fleet. Treat these as planning ranges; your camera gaps and POS estate move the numbers.

| Line | Per store one-time | Per store year-1 run | Notes |

|---|---|---|---|

| Edge AI box (Hailo-8L / Jetson Orin) | $1,200–$2,800 | $240 (support / spares) | Industrial enclosure incl. |

| New cameras (per SCO lane) | $220–$520 | $40 (PoE + maintenance) | Only where overhead view is missing |

| Install + cabling | $1,800–$4,500 | $0 | Local low-voltage contractor |

| Integration / config | $2,500–$5,000 | $1,200 (retrain, support) | First store runs higher |

| Cloud / chain-wide rollup | amortised at chain level | $1,200–$2,400 / store | Warehouse + dashboard |

| All-in per store | ~$8,000–$14,000 | ~$3,000–$6,000 | Custom integrator path |

Compare that to the vendor route. Turnkey self-checkout monitoring commonly runs $80–$180 per SCO lane per month. For a 40-store chain with four SCO lanes each, that is roughly $154k–$346k a year in subscriptions alone — before you add exit, employee and ORC modules. Custom economics tend to overtake the subscription somewhere north of 25 stores, which is exactly the mid-market band driving 2026 adoption.

ROI worked example — a 40-store chain

Let’s do the arithmetic out loud on a representative 40-store grocery chain. This is a model built from the public benchmarks above, not a specific client engagement — your real figure depends on your SCO share, baseline shrink and POS estate. Say the chain does $110M in annual revenue and runs shrink at 2.5% of sales. That is $2.75M lost a year. Assume, conservatively, that AI loss prevention recovers 22% of it, at the low end of the 20–30% band operators report.

Recovery: 22% of $2.75M is about $605k a year. Cost: at roughly $10k one-time and $4.5k annual run per store, 40 stores is about $400k up front plus $180k a year. Year one nets roughly $605k minus $180k run minus $400k build, a small positive; from year two the $400k is spent and the chain keeps about $425k a year. First-store payback lands in the 4–9-month window because a single store carries its own build cost against its own recovered shrink. The chart shows the shape.

Figure 5. A public-benchmark ROI model — per-store cost bars and the cumulative-recovery curve crossing investment near month eight.

The point of showing the maths is that you can run it on your own numbers in five minutes and sanity-check any vendor’s ROI claim. If a proposal cannot survive this arithmetic on your actual shrink rate, it will not survive the board. Want us to run it with your figures? Book a 30-minute call and bring six months of shrink data.

A decision framework in five questions

1. How many stores, and what is current shrink? Under 15 stores, a vendor SCO module on your existing POS is fastest. From 15 to 200, a custom edge build on Hailo or Jetson with chain-specific models is usually right. Above 200, a hybrid of in-house team plus integrator is the durable answer.

2. Which use cases first? Self-checkout and exit theft cover roughly 60% of recoverable shrink in grocery and c-store; receiving adds another 20%. Do not bundle all five at once. Sequence them so the first deployment ships in about 16 weeks and earns the budget for the next.

3. What POS estate? NCR, Toshiba, Square, Diebold-Nixdorf or a regional POS — this layer sets your timeline more than the AI does. Get the vendor data-feed contract reviewed early, before you scope anything else.

4. What is your privacy posture? States with strict biometric law and any EU footprint push you to behavioural-only detection or tightly governed face handling. Make it an architectural constraint on day one, not a footnote at launch.

5. Who triages the alerts? Without a loss-prevention team or a managed SOC that can absorb the queue, the project dies on the operator side no matter how good the models are. Plan the human layer before you sign the build.

Five pitfalls to avoid

1. Cloud inference per camera. The unit economics break above about four cameras. Edge-first is the only shape that scales across a chain without a runaway compute bill.

2. Underscoping the POS integration. The vision side is the easy part. The POS feed is where projects slip by months. Budget 25–35% of the effort here and you will not be surprised.

3. Confronting customers through automation. The system never confronts anyone. The false-positive cost is too high. The operator decides; the software only surfaces.

4. Face recognition without a privacy plan. BIPA and GDPR exposure can dwarf the shrink you saved. Behavioural-only is the safe default; face matching needs consent, signage and governance first.

5. No operator feedback loop. Without a true / false / inconclusive button on every alert, the false-positive rate stays high and staff stop trusting the tool. Build the loop on day one, not in phase two.

KPIs to measure

Quality KPIs. Detector recall above 88% per use case, false-positive rate falling quarter on quarter (target under 15% by month six), end-to-end alert latency under four seconds for self-checkout, and video-clip retrieval above 99.9% for officer review.

Business KPIs. Shrink as a percentage of sales down 15–30% from baseline within 12 months, chain-level payback under 12 months (first store under 9), per-store year-one ROI above 4×, and loss-prevention productivity — cases closed per officer-hour — up meaningfully.

Reliability KPIs. Edge-box uptime above 99.5% per store, camera availability above 99%, model-rollout success above 99.5%, zero privacy incidents chain-wide in the year, and audit-log completeness above 99.9% for anything that could end up in an investigation.

When AI loss prevention is the wrong call

Honesty sells better than a pitch, so here is when to skip this. Single-store independents amortise the engineering poorly — EAS hardware and a basic vendor module will serve you better. Chains with no self-checkout and low baseline shrink (under roughly 0.7% of sales) will struggle to clear the ROI bar. And any operator without loss-prevention staff or a managed SOC to work the alert queue should fix that first, because the models generate leads that a human has to close.

There is also a jurisdictional case. If your privacy regime forecloses even behavioural detection — rare in 2026, but worth checking with counsel — the compliant scope may be too narrow to justify the build. Below about 15 stores or below 0.7% shrink, the maths are tight and the simpler answer is usually the right one. We will tell you that on the call rather than sell you a system you do not need.

FAQ

What is retail loss prevention?

Retail loss prevention is the combination of people, process and technology a retailer uses to reduce shrink — the loss of inventory and cash to theft, fraud and error. In 2026 it increasingly means AI-driven video analytics and point-of-sale exception reporting layered on top of traditional deterrents like EAS tags, locked cases and staff training.

How much does retail shrink cost?

US retail shrink reached $112.1B in fiscal 2022, or 1.6% of sales, in the last full NRF National Retail Security Survey before it was discontinued in 2024. NRF now tracks the trend through its Impact of Retail Theft & Violence report, whose 2025 edition found shoplifting incidents up 18% year over year.

Does AI actually reduce self-checkout theft?

Yes, when it is matched to the POS. Self-checkout loses about 16× more per dollar than staffed lanes (Grabango, 2023), and camera vision that cross-checks each scan against an item-in-bag detection catches the ghost scan and produce-code swap in real time. The alert goes to an attendant within roughly two seconds; the software never confronts the shopper itself.

Is BIPA the only privacy law I have to worry about?

No. Illinois BIPA is the strictest, and its August 2024 amendment now caps accrual at one violation per person, but Texas, Washington and others have biometric statutes, and broader state privacy laws touch surveillance. EU deployments are governed by GDPR Article 9 plus the AI Act. Designing to detect behaviour rather than identity keeps you clear of most of it.

How many cameras per store do I need?

Most grocery stores already run 16–30 IP cameras. A loss-prevention build typically uses 8–14 of them: one per self-checkout lane, the exit door, the dock, and key aisles like baby formula and pharmacy. New installs are usually limited to overhead-per-lane views where the coverage is missing, so you rarely replace the whole fleet.

Everseen or a custom build — which should I choose?

Everseen and other turnkey vendors win for Tier-1 retailers who want a proven self-checkout module with zero engineering. A custom build wins for 25-to-200-store chains where the per-lane subscription crowds out the savings, the use-case mix goes beyond SCO, and the team wants to own alert thresholds, data and the privacy posture. Above roughly 25 stores the custom maths usually turns favourable.

What is the typical payback period?

Roughly 4–9 months on the first store after go-live, and 9–16 months chain-wide once you include the up-front integration and model-training cost. The exact figure depends on baseline shrink, the share of trips through self-checkout, and how hard the loss-prevention team works the new tooling.

Can the system run on our legacy NVR and cameras?

Usually, yes. We pull live feeds over ONVIF or RTSP and treat the NVR as the recorded-storage layer, running the edge AI box alongside it rather than replacing it. We work with whatever VMS the chain already runs — Milestone, Genetec, Avigilon, Hanwha Wisenet, ExacqVision — and some chains modernise the NVR later as part of a broader refresh.

What to read next

Sister pillar

Edge AI video surveillance architecture

The edge-first inference patterns that make per-store AI economics work in retail.

Models

Anomaly detection in video surveillance

The unsupervised side of retail vision — catching behaviour your detector was never taught.

Adjacent

AI video analytics — architecture and ROI

The broader AI-on-video pattern across surveillance, smart cities and retail.

Foundations

Video management systems (VMS) 2026 architecture

The VMS layer the loss-prevention stack lives on top of — cameras, NVR, ONVIF.

Security

AI video analytics for smart security

How the same detection stack extends from retail floors to wider security systems.

Ready to cut shrink 20–30%?

Retail loss prevention in 2026 is a six-layer edge-AI build: cameras, an edge box, YOLO26-class models with a tracker, POS event correlation, a tiered operator queue, and a POS integration that owns the timeline. Five use cases carry the value — self-checkout, exit, receiving, employee and ORC. Detect behaviour, not identity, and BIPA and GDPR stop being a threat. Show the ROI arithmetic on your own shrink, and the board decision makes itself.

The choice that actually matters is buy versus build, and it turns on store count. Under 15, take a vendor module. Between 25 and 200, a custom integrator build usually wins on both economics and control. We’ve engineered video and computer-vision systems since 2005, and we will tell you honestly which side of that line you are on — even when the honest answer is “you do not need us yet.”

Send your shrink data, get a straight ROI read

Free 30-minute scoping call. We’ll size the build, sequence the use cases, and run the payback maths on your real numbers — buy, build or hybrid.