Key takeaways

• Six startup funding options cover almost every software founder in 2026. Bootstrapping, friends & family, angels, accelerators, venture capital, and non-dilutive (grants, RBF, venture debt) — pick the right one for your stage, not the one with the highest cap.

• The MVP cost has collapsed. AI coding tools and a focused dev partner can ship a real software MVP for $25k–$80k — not the $150k–$300k that was standard pre-2024. That changes how much money you actually need to raise.

• The seed bar has hardened. Most institutional seed VCs now expect $500k–$2M ARR before they wire. Below that, target angels, accelerators, or non-dilutive capital.

• AI startups command a big Series A premium. Median AI Series A pre-money is around $84M versus a blended ~$49M overall median (Carta, Q3 2025) — roughly 1.7×; like-for-like, the AI vs non-AI gap is about 38%. Expect it to compress as AI becomes table stakes.

• Cap-table mistakes kill more rounds than bad pitch decks. Stacking post-money SAFEs, skipping the option pool, and giving away more than 25–30% at seed are the common ways founders bury their next round.

Why Fora Soft wrote this playbook

We have been building software products for founders since 2005 — 250+ shipped products and counting. A surprising amount of the conversation in our scoping calls is not about engineering — it is about money. How much do you really need to raise? Should you raise at all? What does the round you are sketching actually buy you?

We have shipped MVPs for founders who funded the build with a single angel cheque, for teams who came out of YC with a YC-standard $500k SAFE, for bootstrappers who paid for development out of early customer revenue, and for grant-backed projects where the funding came from Innovate UK or the EU’s EIC Accelerator. We have watched some of those rounds turn into Series A success stories and others quietly fail because the cap table was already broken on day one.

This playbook is the compressed version of that conversation: the six startup funding options that actually matter for software founders in 2026, when each one fits, what investors expect now versus three years ago, and how to avoid the funding mistakes we keep seeing in our pipeline. Browse our portfolio to see the kinds of products this applies to.

Trying to decide how much to raise and from whom?

30 minutes with a senior engineer who has scoped builds for bootstrapped, angel-funded, and Series A-bound founders. Bring your roadmap; we will tell you what it actually costs.

The state of software funding in 2026

Three things changed materially since the 2022–2023 downturn, and any funding decision you make this year should sit on top of them.

The market recovered, but only at the top. Global venture funding hit a record ~$300B in Q1 2026, and AI took roughly 80% of it — about $242B (Crunchbase, 2026). Four rounds alone — OpenAI, Anthropic, xAI and Waymo — soaked up close to 65% of the quarter’s global capital. If you’re a non-AI software founder, you’re fighting over what’s left, and you feel the squeeze in real time.

The seed bar moved up. What used to be Series A traction (revenue, retention, paying customers) is now the seed-stage entry ticket for institutional VCs. Most tier-1 seed funds want $500k–$2M ARR before they engage. The implication is not “raise less” but “earn the right to raise” with revenue first.

Building got cheaper, fast. Cursor, Claude Code, Windsurf, and a wave of Agent-Engineering tooling have compressed MVP build times by an order of magnitude. A serious software MVP that cost $150k–$300k in 2022 routinely lands at $25k–$80k in 2026 if the team and the partner are good. We walked through these cost levers in detail elsewhere; the short version is that you probably need to raise less than your 2022 mental model suggests.

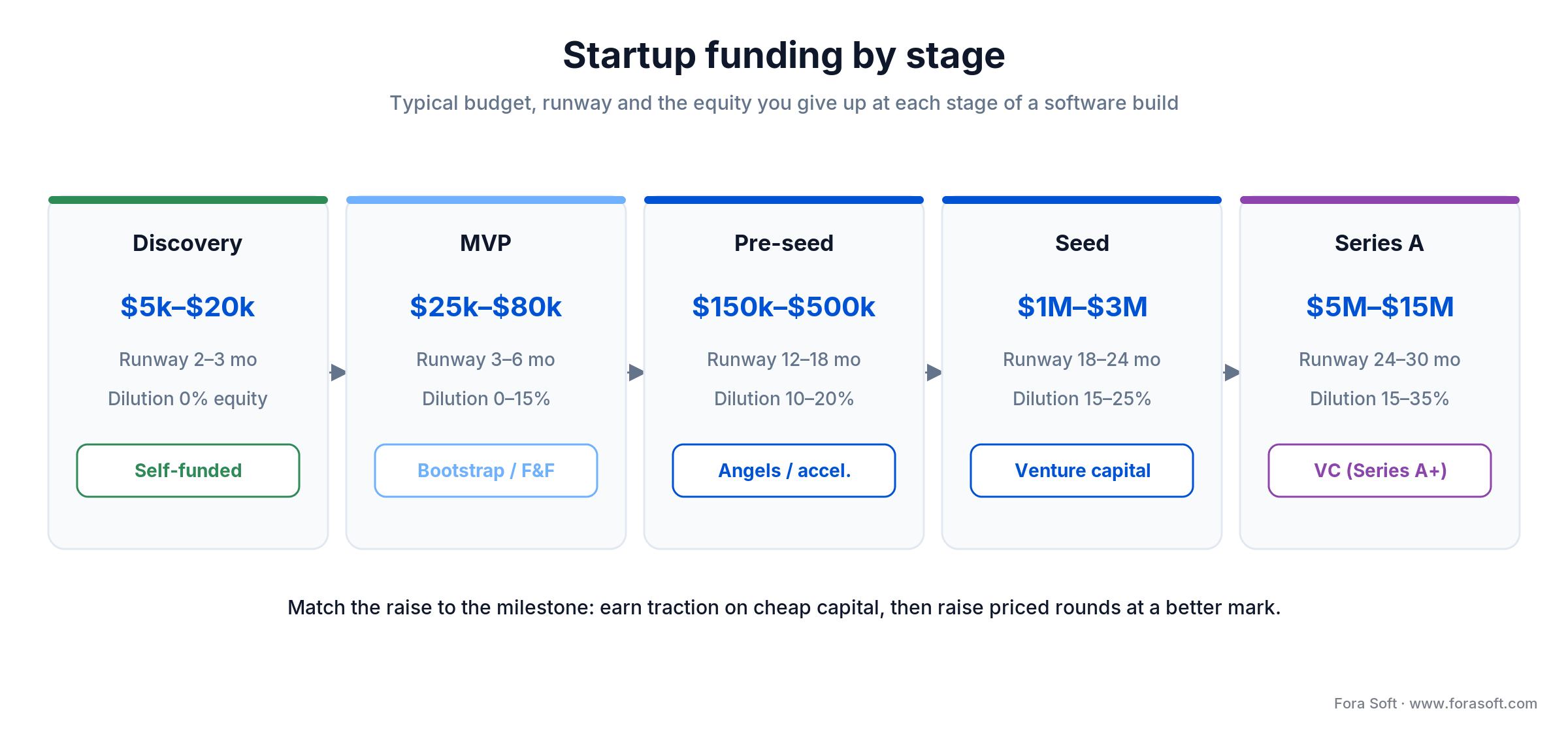

Figure 1. Startup funding by stage — budget, runway and the equity trade-off from Discovery to Series A.

How much money do you actually need?

Before you choose a funding source, get the number right. Most first-time founders raise either too much (and dilute themselves brutally) or too little (and run out of runway six weeks before product–market fit). A simple budget rule:

| Stage | What you actually do | Realistic budget | Runway you should target |

|---|---|---|---|

| Discovery / validation | User interviews, prototype, landing page | $5k–$20k | 2–3 months |

| MVP build | Working product, first 10 paying customers | $25k–$80k | 3–6 months |

| Pre-seed / early traction | $5k–$25k MRR, repeatable acquisition | $150k–$500k | 12–18 months |

| Seed | Hire 3–6 people, scale to $1M ARR | $1M–$3M | 18–24 months |

| Series A | Repeatable GTM, multi-region expansion | $5M–$15M | 24–30 months |

A frequent mistake we see: founders try to raise pre-seed money to skip the MVP stage entirely. Investors at every stage discount that aggressively. Build the smallest possible thing that paying customers will use, then raise on the back of it.

The six startup funding options that fit a software founder

Below are the sources we see funding real software builds in 2026. They are not equally appropriate at every stage; the playbook is to use the right one for the situation rather than chasing whichever has the loudest founders on Twitter.

1. Bootstrapping (and customer-funded development)

Pay for the build out of your own savings or, better, out of money your first customers send you for the product (or a paid prototype). Bootstrapping is no longer a niche move: solo-founded startups — most of them self-funded — climbed from 23.7% of new companies in 2019 to 36.3% by mid-2025 (Carta Solo Founders Report, 2025), and the large majority of startups never raise a VC round at all.

Why pick it: you keep 100% of the equity, you owe nobody a cap-table line item, and revenue forces real user discipline from day one. Combined with AI coding tools, a non-technical founder can ship a meaningful prototype for the price of a few months of one developer’s time.

Limits: growth is capped by the money the business throws off. Capital-intensive markets (consumer apps with paid acquisition, two-sided marketplaces, hardware-adjacent) are very hard to bootstrap. Founders without savings runway need to either pre-sell or raise.

Reach for bootstrapping when: you can build a useful product in 3–6 months on under $50k, have an organic growth motion, and want to delay outside money until terms favour you.

2. Friends and family

An informal first round, typically $25k–$250k aggregate, from people who know you personally. The cheapest capital in terms of paperwork and the most expensive in terms of relationship risk. Use a clean SAFE template (the YC post-money SAFE is the modern default) and document everything.

Why pick it: closes fast, no investor management, and gives you the rope to reach a milestone that triggers a real round.

Limits: creates personal stakes in your professional decisions. Take less than you think you need from people who can actually afford to lose it; never take money from anyone who would feel it disappear.

Reach for friends & family when: you need under $150k to bridge to a real product or first paying customer and you have at least one wealthy supporter who explicitly understands they may lose the cheque.

3. Angel investors and angel syndicates

Individual investors writing $25k–$250k cheques, or organized syndicates (AngelList syndicates, operator collectives) writing $500k–$2M aggregate. Roughly half of US angels invested in at least one solo-founder company in 2024 — far more receptive than institutional VCs, who turn down 75%+ of solo-founder pitches.

Why pick it: angels move fast, often bring domain expertise, and accept SAFE-stage uncertainty. The right operator-angel can open distribution doors no fund will.

Limits: a poorly assembled angel round (12 cheques, no lead, no syndicated pro-rata) creates a messy cap table that institutional investors hate at Series A. Find one or two anchor angels who lead and let them help structure the rest.

Reach for angels when: you have a working prototype or early customers, can describe your wedge in one sentence, and want $100k–$1M of patient capital with industry contacts attached.

4. Accelerators and incubators

Y Combinator runs several batches a year, each with hundreds of companies; the standard YC deal is $500k — $125k for 7% on a post-money SAFE plus a $375k uncapped SAFE with an MFN provision (YC, 2026). Techstars, 500 Global, Sequoia Arc, and a long tail of vertical accelerators round out the field. The selection rate is brutal — YC accepts on the order of 1% — but the platform value (network, demo day, investor pipe) is real.

Why pick it: for first-time founders, an accelerator compresses six months of investor education and network building into 12–13 weeks, and the demo-day round usually closes at a cleaner valuation than you would land cold-emailing investors.

Limits: demo-day fundraising is a frenzy that benefits investors as much as founders; uncapped MFN SAFEs from a YC batch can stack into surprising dilution at Series A. Vertical or regional accelerators vary wildly — some are genuinely useful, some are signaling-only.

Reach for an accelerator when: you are a first-time founder, your wedge is clear, and the network and demo-day access are worth 7% equity at a fixed early valuation.

5. Venture capital (pre-seed, seed, Series A and beyond)

Institutional capital from dedicated VC funds. Pre-seed checks land $500k–$2M on $8M–$15M post-money SAFE caps; seed rounds median around $2–4M; Series A median pre-money hit a record $49.3M in Q3 2025 — about $84M for AI-native businesses (Carta, 2025). US-based companies absorbed 83% of Q1 2026 global venture dollars, so the geographic concentration is real too.

Why pick it: VC is the only path that funds the Series A → B → C scaling that builds a $100M+ revenue business in five years. Top-tier funds bring talent pipelines, distribution, and second-round capital that nothing else replicates.

Limits: the bar is high — serious seed VCs want $500k–$2M ARR; serious Series A VCs want $2–5M ARR with 10–20% month-on-month growth. Below that, you are pitching against companies that already have what you are promising. VC also locks you into a growth-or-die return model that does not fit every business.

Reach for VC when: you have product–market fit, an enormous addressable market, a credible $100M+ revenue thesis in five years, and the temperament for the growth-or-die path.

6. Non-dilutive capital (grants, RBF, venture debt)

The most underused category by first-time founders, and often the cheapest in equity terms. Three sub-options.

Government grants. In the US, SBIR/STTR awards run up to $1.25M for NSF Phase II in 2026 (other agencies vary, and a new Strategic Breakthrough Award reaches $30M). In Europe, the EIC Accelerator put €414M into its 2026 Open call — up to €2.5M grant plus €10M equity per company — alongside Innovate UK and Horizon Europe. Slow (3–6 months to a decision) and paperwork-heavy, but the equity cost is zero.

Revenue-based financing. Pipe, Capchase, Clearco, and Stripe Capital advance you a fraction of your ARR for a fixed fee (typically 6–12%) repaid as a percentage of monthly revenue. Works once you have $500k+ ARR.

Venture debt. Mercury, JP Morgan, and surviving SVB-successor banks lend 25–40% of your last equity round at 10–14% over 36–48 months. Extends runway by 12–18 months without the dilution of a bridge round, but creates fixed obligations.

Reach for non-dilutive capital when: you have either grant-eligible R&D, predictable recurring revenue (RBF), or a recent priced round and want to extend runway without giving up more equity.

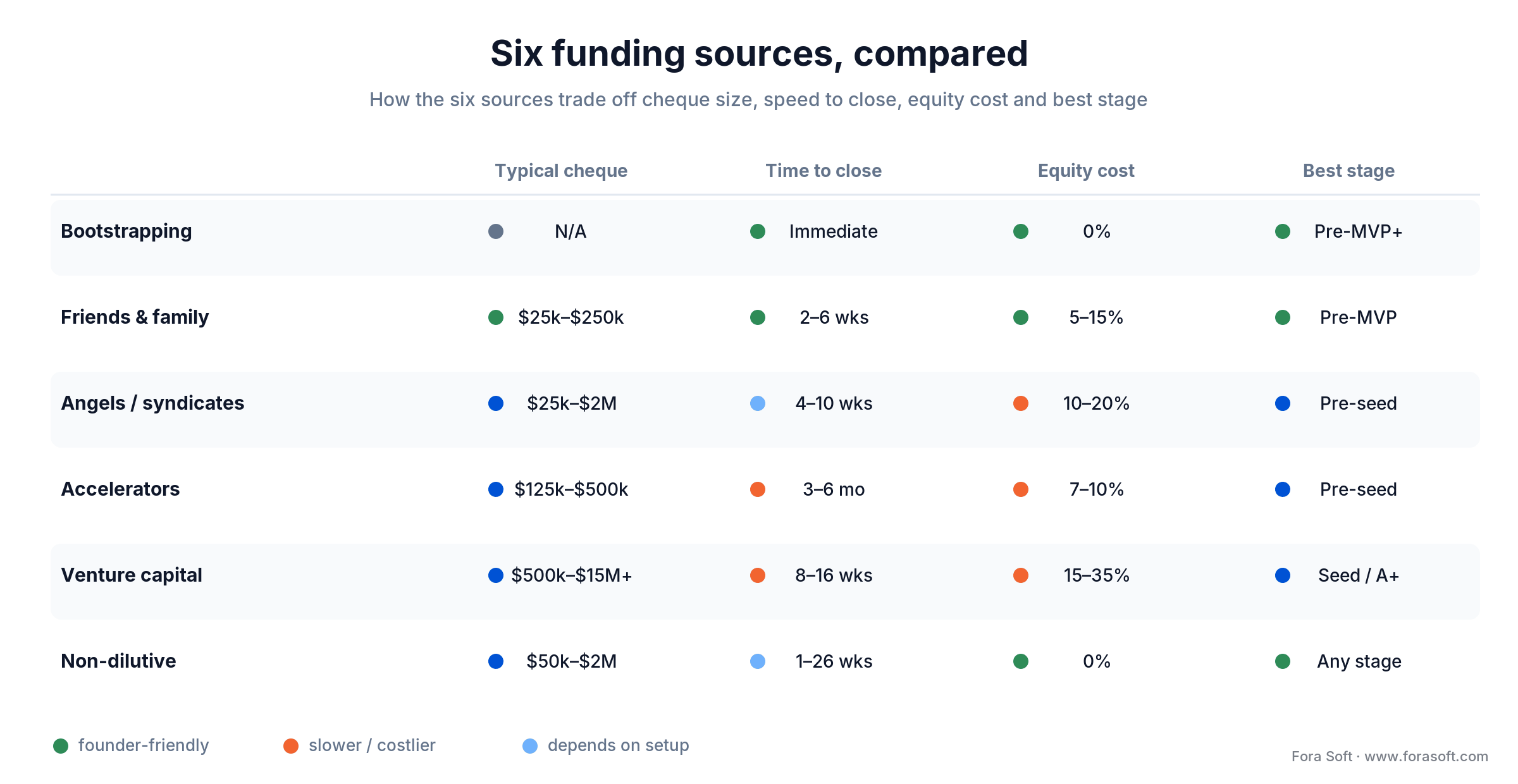

The six sources compared at a glance

| Source | Typical cheque | Time to close | Equity cost | Best stage |

|---|---|---|---|---|

| Bootstrapping | N/A | Immediate | 0% | Pre-MVP through early traction |

| Friends & family | $25k–$250k | 2–6 weeks | 5–15% | Pre-MVP / MVP |

| Angels / syndicates | $25k–$2M | 4–10 weeks | 10–20% | Pre-seed / seed |

| Accelerators (YC, Techstars) | $125k–$500k + network | 3–6 month cycle | 7–10% | Pre-seed |

| Venture capital | $500k–$15M+ | 8–16 weeks | 15–35% | Seed / Series A+ |

| Non-dilutive (grants, RBF, debt) | $50k–$2M | 1–26 weeks (varies) | 0% | Any (grants pre-rev; RBF post-rev) |

Figure 2. The six funding sources compared by cheque size, speed, equity cost and best-fit stage.

What investors actually look at in 2026

VCs spend only a couple of minutes on a first-pass pitch deck before deciding whether to take a meeting. The three slides that move the decision are problem/solution fit, traction, and team — in roughly that order at pre-seed and reversed at Series A.

Problem and solution fit. One sentence on the pain you solve, one on why your product is the way to solve it, one on why now. Vague TAM slides and “we’re Uber for X” framings end the meeting before it starts.

Traction. Real numbers in the order investors weight them: paying customer count, MRR/ARR, month-on-month growth, retention/churn, payback period. Vanity metrics (downloads, sign-ups) get discounted to zero. 10–20% MoM growth is the threshold that makes investors lean in.

Team. Domain expertise, prior shipping experience, and the founder’s ability to articulate the next 18 months in three milestones. Solo founders are not disqualifying but raise an obvious question that your deck must answer.

The AI angle. If you are AI-native, lead with proprietary data, model architecture, or a real efficiency edge. If you are not, do not pretend — investors prefer an honest non-AI thesis to a tacked-on “and we use ChatGPT” bullet.

Need a tighter MVP scope to fit your raise?

We help founders cut MVP scope to the smallest thing that proves the thesis — usually trimming 30–50% of the planned budget without losing the story.

Cap table discipline — the founder skill nobody teaches you

Most failed software fundraises we see do not fail because the product is bad. They fail because the cap table is. Three rules to internalize before you sign anything.

Always model fully diluted ownership. Outstanding-share math hides the option pool, the SAFE conversions, and the warrants that all dilute you on the same day at Series A. Build a fully-diluted spreadsheet from day one.

Watch the post-money SAFE stack. Post-money SAFEs lock in the investor’s percentage. If you raise three SAFEs at $5M, $8M, and $12M caps over 18 months, all of them dilute you when the priced round converts — not just the latest one. Stack one or two carefully; do not stack five.

Mind how the option pool is sized. A pool carved out of the pre-money valuation dilutes only you and your existing shareholders — not the incoming investors. That is the “option-pool shuffle,” and it is the trap to watch. Keep any pre-money pool no bigger than your real 12-month hiring plan justifies, and push to have new options counted in the post-money so the fresh capital shares the dilution.

A founder team should expect to retain 50–60% after a clean Series A. Below 40% by Series A is a red flag for follow-on investors and signals one of those mistakes was made.

Term sheet basics for non-lawyers

You do not need to be a lawyer to negotiate a term sheet, but you do need to recognize the four terms that matter more than the headline valuation.

Liquidation preference. Standard 2026 default is 1× non-participating preferred. Anything above that — 1.5× or 2× participating — means the investor takes 1.5–2× their money before founders see anything in a sale, then participates pro-rata in the remainder. Walk away from participating preferred unless you absolutely have to.

Anti-dilution. Weighted-average broad-based is the founder-friendly default. Full-ratchet anti-dilution resets the investor’s price to whatever the next (lower) round is, devastating founder equity in a down round. Do not accept full-ratchet at Series A.

Vesting. Standard founder vesting is 4 years with a 1-year cliff, often with credit for time already worked. Refusing to vest on the founder side reads as a red flag. Insist that any acceleration on change-of-control is double-trigger (sale + termination) rather than single-trigger.

Board composition. Series A typically gets one investor seat. Two founders + one investor + one independent = a healthy four-person board. Avoid configurations where the lead investor controls a majority.

A funding-friendly software development partner

A pattern we keep seeing work: instead of raising a round to hire 4–6 in-house engineers and pay them for 12 months before you have a product, raise a smaller round and contract a focused development partner to ship the MVP and the first iteration on it. The math is straightforward.

A senior engineer on US payroll runs $180k–$250k all-in per year. Four of them for nine months is roughly $700k before you ship anything users pay for. The same scope, delivered by an experienced product team using Agent Engineering, lands much closer to $80k–$200k for an end-to-end MVP plus its first production iteration (a focused single-flow MVP is the cheaper $25k–$80k band from earlier). You can hire your in-house engineers later, against post-traction equity, with much less dilution.

The right partner is not a body shop — you want product thinking, deployment ownership, and a clean handover so you can take the codebase in-house when you raise. That is what we built our AI integration and product delivery practice around for exactly this reason. If your product is video, streaming, or AI-heavy, our engineers publish the deep technical playbooks behind that work in our streaming engineering library.

How AI and Agent Engineering changed the math

Two things shifted in the last 18 months that change what your fundraise should pay for.

MVP cost dropped sharply. Cursor, Claude Code, and Windsurf take a big bite out of early-stage greenfield effort. We use Agent Engineering throughout our own delivery, which is why our quotes for an MVP are usually 30–50% lower than the same scope two years ago. The implication for fundraising: a $200k pre-seed cheque now buys what a $300–400k pre-seed cheque bought in 2022. Raise less, dilute less, hit the milestone, raise the next round at a better mark.

Investors price in leaner teams. If you are pitching seed with a 12-person engineering team and a $4M annual burn, sophisticated investors will ask why you cannot do the same with five engineers and Agent Engineering. We walked through that math in detail elsewhere; the short version is that the new default is leaner founders, faster shipping, and earlier revenue.

Geographic differences worth knowing

United States. Still the deepest pool by an order of magnitude — 83% of Q1 2026 global venture dollars went to US-based companies. Tier-1 hubs (SF, NYC, Boston) carry the highest density and the highest valuations. Secondary hubs (Austin, Miami, Denver) have grown materially and are easier to break into for first-time founders.

UK and Europe. Capital is thinner than in the US but grants are stronger. Innovate UK, Horizon Europe, and the EIC Accelerator (€414M in its 2026 Open call) make non-dilutive money a real option. UK-based founders incorporating in Delaware in parallel is increasingly common when targeting US institutional capital.

MENA. The fastest-growing region: H1 2025 startup funding hit $2.1B across 334 deals, up 134% year-on-year, with Saudi Arabia alone taking $1.34B (fintech-led) on the back of PIF and other state-backed capital. Founders with regional anchors should not ignore this pool.

APAC. Singapore concentrates the majority of Southeast Asia’s startup funding as the region’s incorporation hub; China still leads the wider region. Cross-border raises into APAC require local relationships that take 6–12 months to build.

KPIs investors look at — and the thresholds that matter

Quality KPIs. Month-on-month revenue growth above 10% (15–20% gets investors excited). Net revenue retention above 100% for SaaS, above 110% for enterprise. Gross margin above 70% for software. Logo retention above 90% annually.

Business KPIs. CAC payback under 12 months for SMB SaaS, under 18 months for enterprise. LTV/CAC ratio above 3. ARR per FTE above $150k at seed, above $250k at Series A. Burn multiple (net burn / net new ARR) under 2 at seed, under 1.5 at Series A.

Reliability KPIs. Cash runway disclosed openly (12+ months at the time of pitch). Founder equity above 50% post-Series A. Clean cap table with documented vesting and option pool. Audit-ready financials from day one — investors who like the deck still walk away from a messy data room.

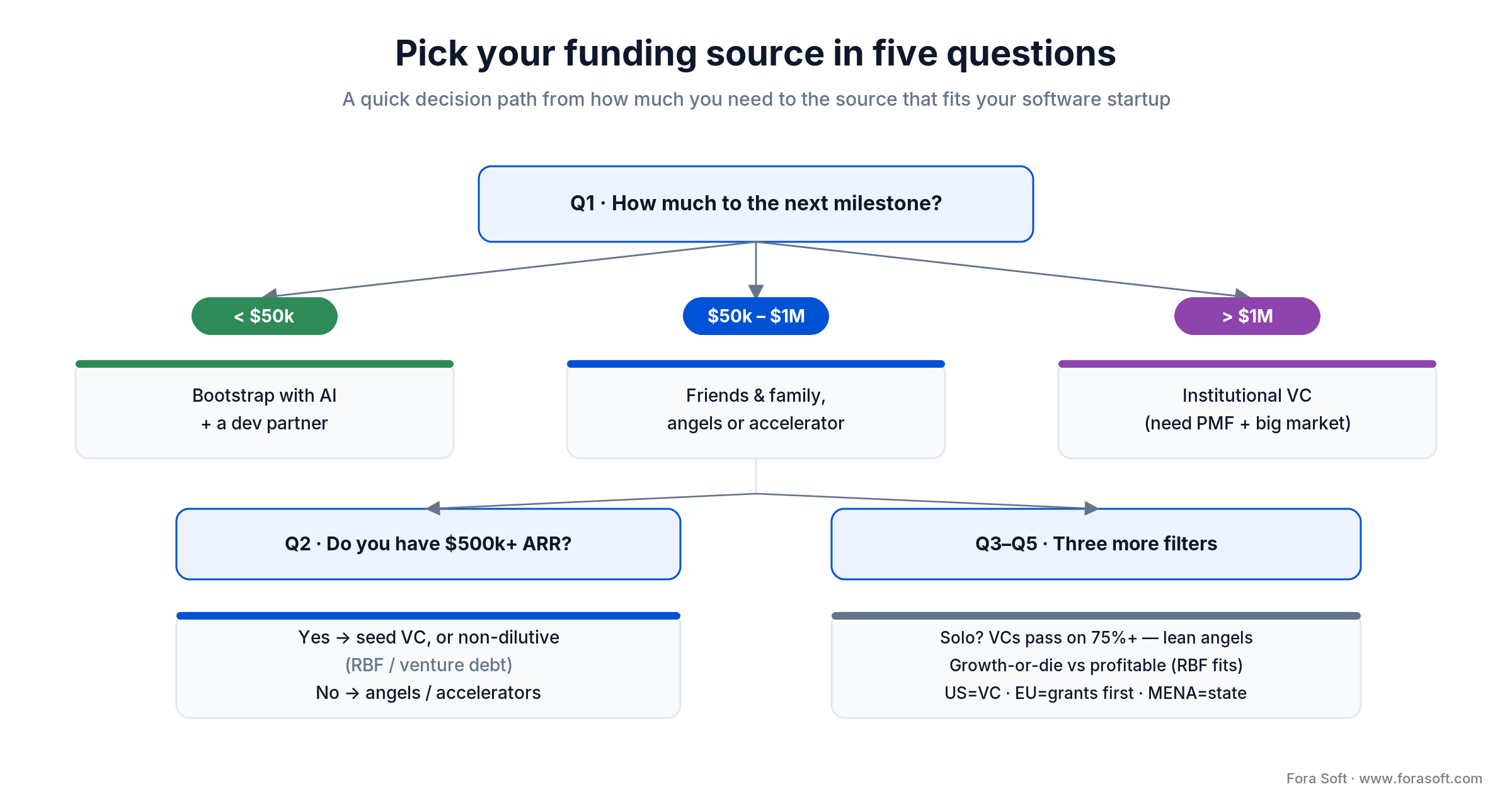

A decision framework — pick your funding source in five questions

1. How much money do you actually need to reach the next real milestone? If under $50k, bootstrap with AI tools and a focused dev partner. Under $250k, friends & family or a single anchor angel. Above $1M, you are talking institutional VC.

2. Do you have $500k+ ARR? If yes, you can credibly approach institutional seed VCs and consider non-dilutive options like RBF or venture debt. If no, raise from angels or accelerators while you get there.

3. Are you a solo founder or a team? Solo founders raise on average 60% less from VCs and face a 75%+ rejection rate at institutional funds. Angels and accelerators are more receptive. Plan accordingly or hire a co-founder before Series A.

4. Is your business growth-or-die or sustainably profitable? VC requires the former. If you are building a sustainable software business with 30–50% YoY growth, RBF and venture debt let you scale without committing to the 10× outcome treadmill.

5. Where are you geographically? US founders default to VC and angels. EU founders should always check grant eligibility first. MENA-anchored founders should explore sovereign and family-office capital. None of these is exclusive; the smartest stacks combine two or three.

Figure 3. A five-question decision path from how much you need to the source that fits.

Five fundraising mistakes that kill software startups

1. Raising too early. The number-one reason seed rounds fail is lack of traction. Build to $25k–$100k MRR before approaching institutional money. Investors at every stage discount pre-traction pitches aggressively in 2026.

2. Pitching the wrong investor for your stage. Series A funds do not lead pre-seed rounds; angels do not write Series A cheques. Match the cheque size, fund size, and stage thesis before you pitch. The wrong meeting wastes everyone’s time and burns your warmest reference.

3. Stacking post-money SAFEs without modeling Series A dilution. Five $250k SAFEs at incrementally rising caps look harmless until they all convert at the priced round and you discover you sold 30% of your company before the lead even showed up.

4. Wrong jurisdiction. If you intend to raise US institutional capital, incorporate as a Delaware C-Corp from day one. Restructuring out of a UK Ltd or an Estonia OÜ into Delaware mid-fundraise wastes 2–3 months and several thousand dollars in legal fees.

5. Confusing capital with progress. Closing a round is not a milestone. Shipping a product customers pay for is. Founders who treat the announce-on-TechCrunch moment as the win burn through the cheque without moving the underlying metrics.

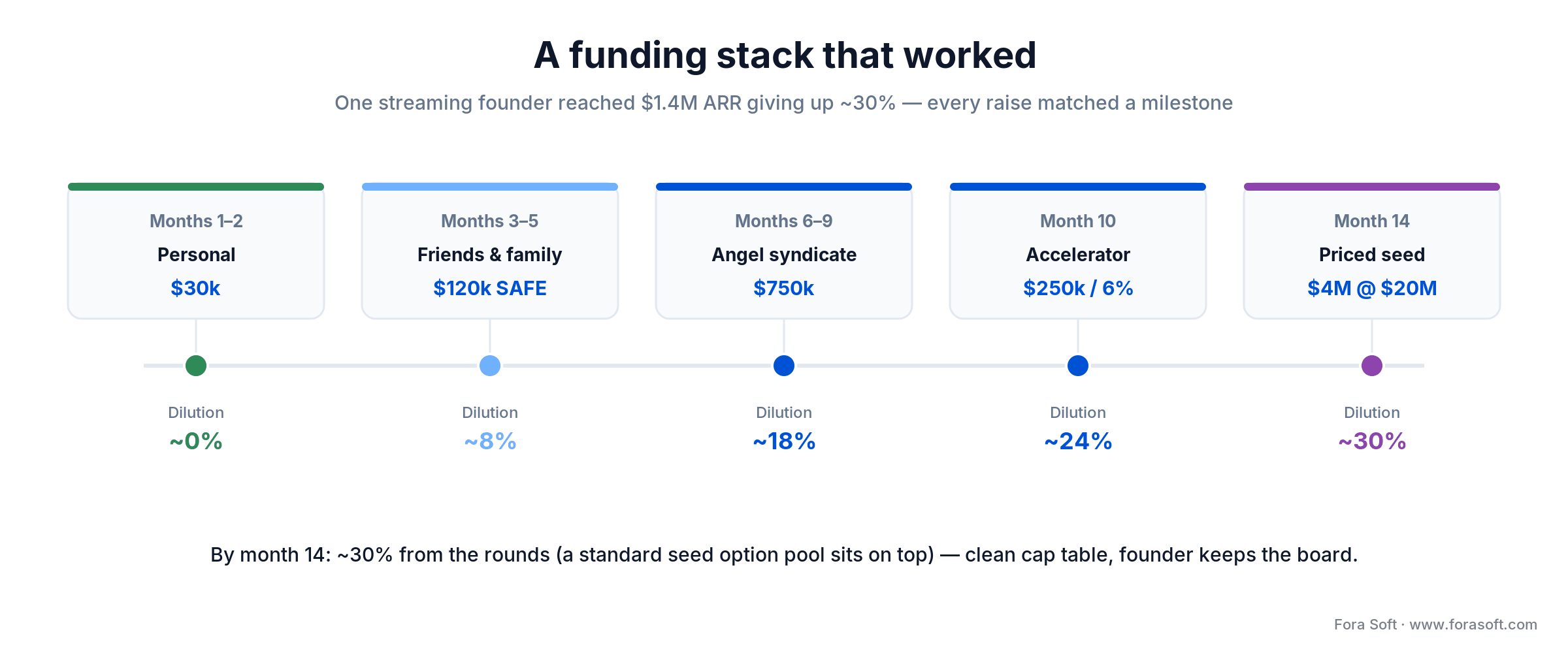

Mini case — a stack that worked

A recent founder we worked with had a streaming-platform idea, $30k of personal savings, and no investors. Their funding stack ended up being a clean illustration of the right pattern.

Months 1–2: $30k of personal capital plus our scoping work to ship a discovery prototype and validate with 12 paying design partners. Months 3–5: a $120k friends & family round on a YC-standard post-money SAFE at an $8M cap, paying for the MVP build (we delivered it for ~$70k using Agent Engineering, leaving $50k of operational runway). Months 6–9: $12k MRR and a clean retention curve led to a $750k angel-syndicate round on a $14M cap, lead-angel introduced via two design partners. Month 10: applied to and accepted into a vertical accelerator with another $250k for 6%, primarily for the network. Month 14: $1.4M ARR and a $4M priced seed round at $20M post led by a tier-2 fund.

Founder dilution by month 14 came to about a third from the rounds themselves, plus the standard ~10% option pool the priced seed added — still a clean cap table, and the founder kept board control. The stack worked because every step matched the actual milestone, not the founder’s ego.

Figure 4. One founder’s funding stack: each raise matched a milestone — ~30% dilution from the rounds (option pool on top) by $1.4M ARR.

Want a similar staged plan for your build? Grab a 30-minute slot and we will sketch a funding/build plan against your specific roadmap.

2025–2026 funding trends every founder should price in

Family offices became a real direct-investment layer. More family offices now write cheques straight into startups instead of only backing funds as LPs. Founders with relationships in this segment often have a faster path to $1–5M cheques than cold-pitching tier-1 VCs.

Sovereign wealth in tech. Saudi PIF and UAE Mubadala are deploying billions into AI and fintech, and the cheques are getting written into Series B and later rounds for European and US founders. If your business has a credible MENA expansion thesis, the introduction is worth pursuing.

Mega-fund retreat. Tiger Global, SoftBank Vision Fund, and Coatue have all materially scaled back. Capital is concentrating into fewer, higher-conviction bets. Spray-and-pray is over for now.

Token funding came back. Crypto and Web3 fundraising rebounded through 2025, with milestone-based grants gaining credibility over all-or-nothing token launches. Worth knowing about; not worth pursuing unless you are building infrastructure that genuinely needs token economics.

Solo founders are fundable but capped. The share of solo-founded startups rose from 23.7% (2019) to 36.3% (mid-2025), yet solo-led companies pulled only 14.7% of priced-round cash in 2024 (Carta, 2025). Angels back solo founders about 48% of the time; VCs pass 75%+ of the time, and solo founders raise on average ~60% less than founding teams. Plan accordingly.

When NOT to raise outside money at all

Not every software product needs venture capital. Skip outside money entirely when your business has a clear path to $200k–$1M ARR within 12 months on bootstrapped resources, when your customers will pay you upfront for the build (the cleanest funding source of all), or when your unit economics are already healthy and you can reinvest cash flow into growth.

Take outside money when capital actually buys something you cannot get without it — rapid GTM expansion, a regulated certification, hardware, an enterprise sales team. The only good reason to dilute your equity is to fund a step-change you would not otherwise reach in time.

FAQ

How much money do I really need to launch a software product in 2026?

For a focused MVP that paying customers can use, $25k–$80k is realistic in 2026 with the right partner and AI tooling. Add $10k–$50k for the first six months of marketing and sales, and you should target $50k–$150k of pre-seed funding to reach early traction. The exact number depends on whether you are paying yourself, your domain’s complexity, and your acquisition motion.

Should I bootstrap my software startup or raise from investors?

Bootstrap if you can reach $200k–$1M ARR within 12 months on personal capital and customer revenue, and if your business does not need a step-change to win its market. Raise if capital buys something you cannot get otherwise — rapid GTM, hardware, regulated certification, or scaling against a well-funded incumbent. The two are not mutually exclusive; many of the best software founders bootstrap to first revenue, then raise on much better terms.

What is the difference between angel investors and venture capitalists?

Angels invest their own money in cheques of $25k–$250k, usually at pre-seed and seed stages, and decide quickly. Venture capitalists invest a fund’s money on behalf of limited partners, write $500k–$15M+ cheques starting at seed or Series A, and have stricter return requirements. Angels are more flexible on stage and traction; VCs come with portfolio support, follow-on capacity, and signaling power.

Are accelerators like Y Combinator worth the equity?

For most first-time founders building venture-scale software products, yes. The $500k YC standard deal — $125k for 7% plus a $375k uncapped MFN SAFE — is a fair price for the network, demo-day visibility, and 12 weeks of intense product/sales coaching. The acceptance rate is roughly 1%, so plan for it as a stretch outcome alongside other paths. Vertical and regional accelerators vary widely in quality — check the alumni outcomes before committing equity.

Can I get government grants for a software project?

Yes, especially if there is a research, AI, or deep-tech angle. SBIR/STTR grants (US) award up to ~$2M across phases. Innovate UK funds dozens of software projects per year. Horizon Europe and the EIC Accelerator support European founders with substantial non-dilutive capital. Grants take 3–6 months from application to decision and require detailed project plans, but the equity cost is zero.

What is revenue-based financing, and when should you use it?

Revenue-based financing (Pipe, Capchase, Clearco, Stripe Capital) advances you a fraction of your annual recurring revenue for a fixed fee, typically 6–12%, repaid as a percentage of monthly revenue. It works well once you have $500k+ ARR and predictable revenue. The advantage over equity is zero dilution; the disadvantage is fixed repayment that bites if growth slows.

Where should I incorporate my software startup?

Delaware C-Corp is the default if you plan to raise US institutional capital. UK Ltd is fine if you stay UK-only and rely on Innovate UK and EIS schemes. Estonia OÜ is excellent for bootstrapped, profit-reinvesting businesses. Many international founders incorporate in their home jurisdiction and add a Delaware C-Corp parent before raising US VC; doing it from the start saves 2–3 months of restructuring later.

How much equity should I give up in my first round?

Aim to keep dilution at the seed stage to 15–25% of fully diluted equity. Pre-seed stacks (friends & family + angels) typically take 10–20% combined. Founders should hold 50–60% post-Series A; below 40% is a warning sign for follow-on investors. Always model fully-diluted ownership including the option pool, not just outstanding shares.

What to Read Next

MVP

Why Cut Features and Launch the Product Early

The classic MVP discipline: ship the smallest thing that proves the thesis.

Cost

How to Cut Costs on Your Software Project

The levers that make a $300k MVP cost $80k without losing scope.

GTM

Selling a Product: How to Get Your First Paid User

The early-traction playbook investors actually want to see in your deck.

AI build

How to Build Apps with AI in 2026

A non-developer’s honest playbook for shipping software with AI tools.

Ready to fund your software product the right way?

Funding a software product in 2026 comes down to choosing among six startup funding options. Bootstrapping is more viable than ever; angels and accelerators carry pre-seed; institutional VC owns seed and beyond; non-dilutive capital extends runway without diluting equity. The founders who win do not chase whichever round is loudest; they pick the source that matches the actual milestone, raise less than they think they need, and protect the cap table from day one.

If you are scoping a build and trying to figure out how much to raise and from whom, we have done this enough times to skip the survey phase. Bring a roadmap, a budget, or just a sketch — we will tell you what we would do.

Let’s pressure-test your funding plan

30 minutes, one senior engineer, zero fluff. We will help you size the build to the round you can actually close.